Published: 17 Aug, 2021 CET.Updated: Tue 17 Aug 2021 16:26 CET

Here's our tips for getting the best energy deal in Norway. Photo by Fré Sonneveld on Unsplash "

The average price of electricity for households in Norway is more than three times higher than the same time last year. Here are The Local's tips for getting the best bang for your buck.

Advertisement

A new analysis and market comparison from data collection firm Statistics Norway has found that the cost of electricity for households excluding taxes and grid rent was 50.9 øre per kWh in the second quarter of 2021.

This is three times higher than the same period last year. In its quarterly report, the Norwegian Water Resources and Energy Directorate (NVE) emphasised that higher fuel prices in Norway and increasing costs in the European market were behind the rises.

When considering grid rent and taxes, the average price of electricity in Norway was 116.1 øre kWh.

Advertisement

What type of arrangements offers the best deal?

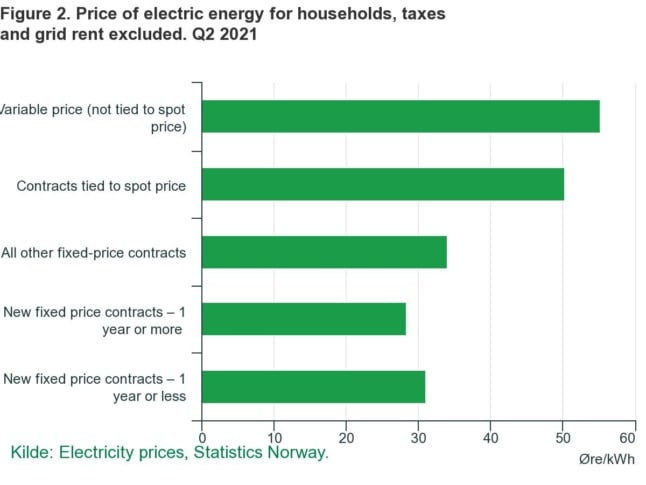

Households with fixed-price contracts paid on average the lowest prices for electricity in the second quarter of this year. The cost of a new fixed-price contract that lasts a year or less was around 50.3 øre per kWh when including taxes and fees. This is around roughly half the average that Statistics Norway reported. Surprisingly only 2.5 percent of homes in Norway have a fixed price contract despite the lower prices.

Those with a new fixed price contract taken up during Q2 that will run for more than a year get a slightly better deal than those with a fixed price contract that will last for a single year or less.

You'll be able to see which arrangements cost what in the graph below.

Electricity prices according to arrangement. Source: Statistics Norway

Due to the rising prices, those with variable contracts, either tied to the spot price or not tied to a spot price, paid more.

A spot price contract, sometimes called purchase price or market power agreement, is calculated daily by the Nordic power exchange Nord Pool. Under a spot price agreement, customers pay the same price as the electricity supplier but instead pay a surcharge and fixed monthly price to the energy company.

Advertisement

Tips for getting the best deal?

The best deal isn't always what looks like the cheapest on paper. For example, fixed-price contracts are traditionally pricier than spot contracts. However, a fixed-price deal can be ideal for many on freelance contracts or who like to work within a budget as you know your monthly energy bill will be the same.

This is vital for many as prices can fluctuate massively between the winter and summer when more energy is needed to heat homes as temperatures plummet into the minuses.

In addition to this, as prices are expected to rise throughout the rest of 2021 through 2022 following low prices in 2020, it may be best to sign a fixed-term agreement for a year to try and stay ahead of the curve should prices skyrocket in the winter.

Typically, though, if you don't need to keep a tighter eye on your outgoings and you're OK with the idea of the prices varying throughout your contract, then a spot contact could offer the best overall value.

In most cases, these wind up being cheaper because they pose the least risk to electricity companies profit margins as you are paying the same price they are in addition to the surcharge, which guarantees a profit for the companies.

Shopping around is also essential wherever you are, and Norway is no different. However, if you want to get the best deal where you are, it's best to use a comparison site such as strøm.no. Comparison sites let you compare the different types of agreements and offer you a price based on where you live, how much energy you use, and your property's size. Shopping around on comparison sites can save you thousands of kroner a year.

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Electricity prices according to arrangement. Source: Statistics Norway

Electricity prices according to arrangement. Source: Statistics Norway

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.